.svg)

Author: Mikkel A Thomassen, Partner, Smith Innovation

In April 2025 the second round of the CBC Open Call was launched. This was an opportunity for CBC to support 6 winning Blueprint Projects with €70,000 funding as well as network and market access support. CBC framed the Open Call around three key challenge areas, and were looking for organisations that addressed one or multiple of the topics.

The challenge areas were: organisations demonstrating market assurance on the quality of secondary materials, or organisations showcasing value of secondary materials, or finally organisations unlocking data and information flows across the value chain to facilitate and implement material reuse and recovery.

The objective of the Open Call and the selection of these key challenge areas was to accelerate circular solutions in the built environment, through the support of real-world solutions that are ready to be scaled.

In the 2025 Open Call CBC received 88 applications. Besides being a strong cohort for identifying 6 winners ultimately, the cohort also gives a current view of the entrepreneurial landscape for Circularity across Europe in 2025. So what patterns did we see in the cohort?

The majority of the applications were based in Northern Europe and were targeting a Northern European market. There is a strong bias in the networks of the organisations involved in CBC towards this part of Europe, therefore this is not necessarily unexpected, nor truly indicative of a larger market here than elsewhere. Nonetheless, it is a reminder that the pace towards circularity is not equal across Europe and that the challenge is to “innovate across” rather than starting anew in each country.

The applications differed in many ways including the materials and parts of the building they focused on, how they envisioned change would happen and what final solution they were aiming for. However there were overlaps in key themes of applicants which we have simplified into three key clusters within the cohort.

Fit-out and interior solutions were a dominant product category, but there was an equally strong interest in load-bearing structures. Windows, insulation and HVAC solutions were addressed but this is an area that requires more attention in light of the EU Energy Performance of Buildings Directive, which necessitates upgrades to buildings with poor energy performance by 2050.

In this cluster solutions focused on improvements to products, product receipts and the associated testing and documentation. The typical output of these solutions were physical products.

This cluster of applications, often driven by organisations rather than private companies, were concerned with how the industry or specific value chains can collaborate and make change possible and profitable across the interest of any single actor.

Key focuses of solutions in this cluster were, value chain reconfigurations, new business models for business and ownership (building-as-a-service included), plus performance-based contracts. The outputs were often envisioned as a roadmap for the industry or a roadmap for collaborative buy in from actors within a specific value chain.

In this cluster the focus of applicants were digital solutions that enabled market transparency, data generation or data-integrated systems, often AI-assisted. Examples of the digital solutions included digital market platforms to create better data transparency, or secondary material identification platforms to provide greater data availability, or decision-making tools with integrated data, such as BIM-models.

In this cluster the outputs were typically software tools, digital protocols or a digital market platforms.

Of course, these three clusters do not fully represent all applications. For instance, we saw a large group of design- and client-driven projects aiming to test out circularity on 1:1 building projects as well as more university-driven applications with the aim of making research knowledge widely available to the industry. Also projects investigating improving worker skills and involvement by targeted training and participatory design.

Taken altogether, the applications were a testimony that the market for circularity is still in the making rather than being fully mature - as we know it for non-circular solutions. Rather than seeing applications purely from commercial companies working on their own, we saw applications from actors representing value chains and the industry as well as research-driven projects providing the knowledge, standardization and testing methods needed to make market transactions flow.

In other words, we saw that the applications do not only try to mature solutions (supply) and engage customers (demand) but also and in particular try to facilitate the intersection of supply and demand (the marketplace). In this perspective, it’s clear that the applicants are attempting to navigate a circular sector that is beyond initial research and early customer explorations but is not fully at the stage where it can be driven by commercial interest of single market players. It is therefore clear to us, that making the connection between research push and market pull is where CBC and other collective initiatives can make a difference.

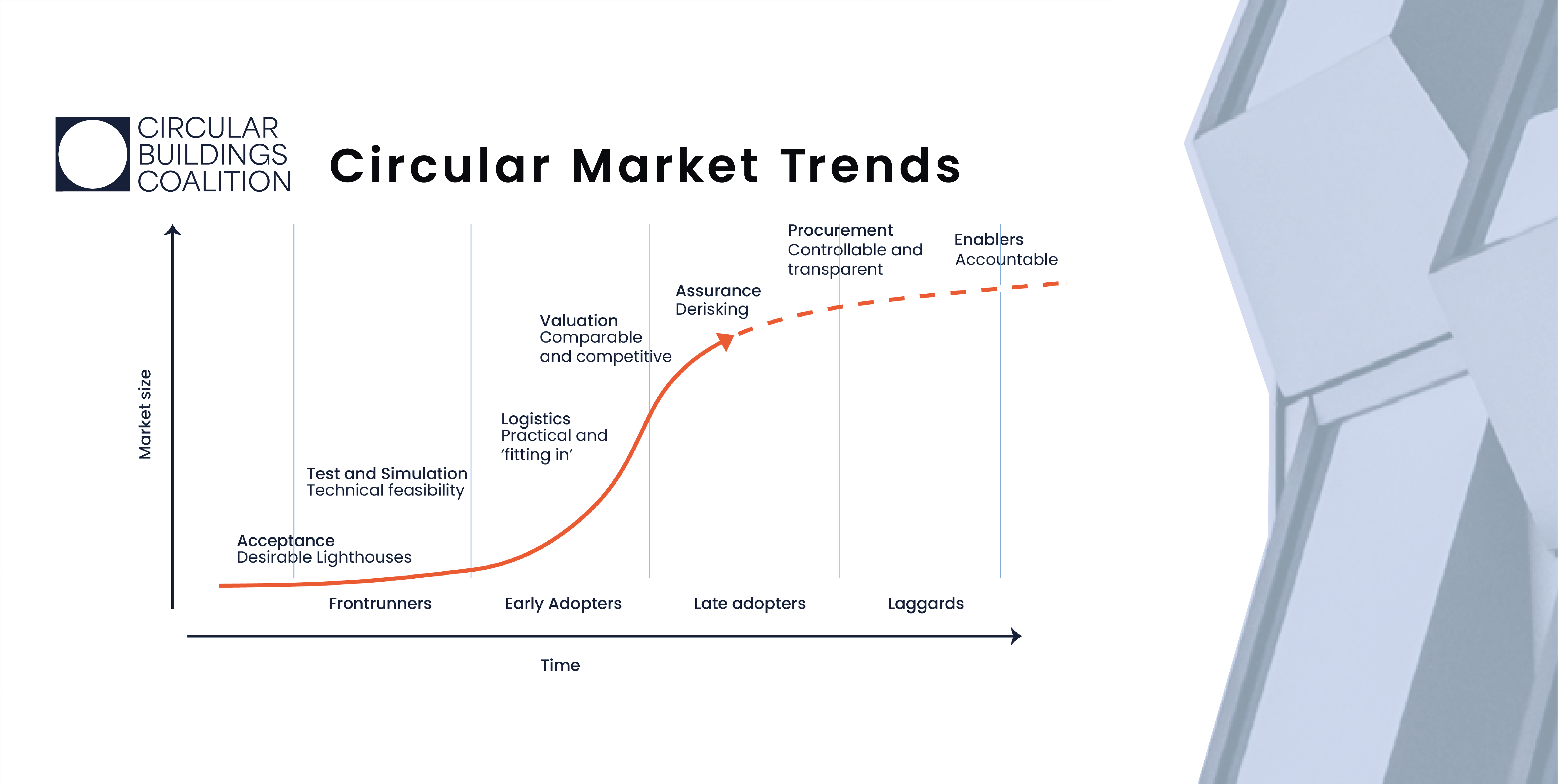

Where to next? What is the current status and where could CBC and other circular leveraging initiatives go next. Based on our learnings from the CBC publications and the 2024 and 2025 Blueprint Project cohorts, our understanding is that a developed marketplace that reduces cost and risks related to circular solutions, and which showcases their value in being circular, is what is most critically lacking.

Looking across the 88 cohort, seven market structures need to be in place for circularity to grow (see graph at top of article):

- Acceptance. Where circularity is considered meaningful and desirable for customers as well as the people providing it.

- Test and modelling for technical feasibility: where we can prove solutions function in their intended ways.

- Logistics: Resolving the practical aspects of handling materials from demolition via intermediaries to a new site, plus knowing how to build with the secondary materials

- Valuation: The ability to make circular solutions comparable and competitive against other solutions for the client and their subcontractors to justify the circular choice.

- Assurance: The ability to de-risk circular solutions by insurance, warrants, and integrated business models.

- Procurement and contracting: The ability to make circular solutions part of tendering and subsequent contracts in ways that make circular ambitions core to the projects.

- Financial enablers: How circular solutions can be promoted by financial schemes and building stock assessments that give a premium to circular solutions.

As a working hypothesis, these seven market enablers might be categorized by different levels of risk-willingness of customers. For the few frontrunners it is enough that the solutions are desirable and that technical feasibility can be proven at a very basic level. For early adoptors, practical concerns related to logistics and valuation also plays an important role, whereas derisking, proven procurement models and even a financial premium is essential to include all market segments.

As we in CBC try to showcase how success looks when circular principles are fully applied, this analytical scheme also suggests important pointers for the next phase of CBC for circular solutions across products, building typologies and geographies, namely that we would like to test and document models for:

- assurance

- procurement

- enablers (investment)